Why The Government Lies About Inflation

![]()

Albert Einstein understood how money and interest worked better than almost anyone who never worked a day on Wall Street.

Compound interest is the 8th wonder of the world. He who understands it, earns it; he who doesn’t, pays it.

This wasn’t just because he was Einstein. This was because he understood Special Relativity.

In 1905, Albert Einstein determined that the laws of physics are the same for all non-accelerating observers, and that the speed of light in a vacuum was independent of the motion of all observers. This was the theory of special relativity.

So why even discuss “c” (speed of light in a vacuum)? Because you need to establish a gauge. Why care about a gauge in physics? So you can actually measure the impact of the laws of physics when different observers are accelerated at different rates. Which brings us around to how Einstein intuitively understood who ate whom when it came to financial machinations. Economics, like Physics can only be understood through an effective Theory of Metrication. You need a butt-kicking gauge.

Gauge theory, class of quantum field theory, a mathematical theory involving both quantum mechanics and Einstein’s special theory of relativity that is commonly used to describe subatomic particles and their associated wave fields. In a gauge theory there is a group of transformations of the field variables (gauge transformations) that leaves the basic physics of the quantum field unchanged. This condition, called gauge invariance, gives the theory a certain symmetry, which governs its equations.

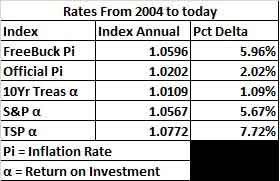

The same can be said for measuring the impact of interest on monetary resources. Here we see a set of 3 rates running from 2004 to present. This time period is chosen so that I could run all three chosen indexes over an equal span of time. The two inflation rate are the Official CPI-U and the Freebuck.com Homebrew Inflation Index. The three rates of return are The 10-Yr UST Bond (used as a benchmark for Fed Policy and mortgage rates), the index price for the S&P 500, and the returns an index of funds available with the Federal Government Thrift Savings Plan Pension Funds. These annualized rates follow below.

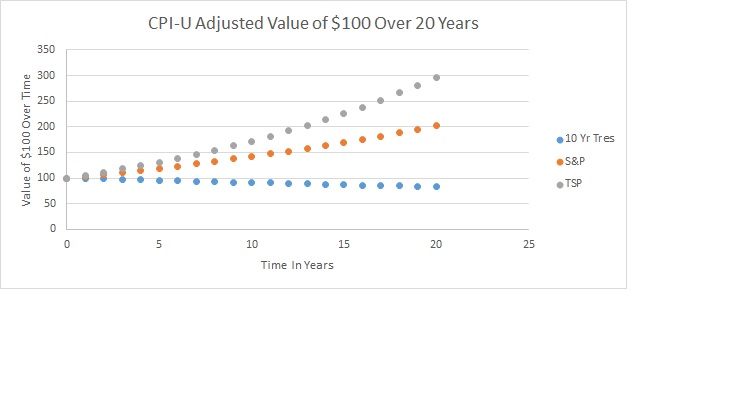

Here we can see what happens if we take $100 in 2021 and compound it for 20 years by each rate of return for 10 Year T-Bills, The S&P and The TSP Pension Fund.

Using this chart with no reference to inflation lets you make all sorts of fun claims if you work for The New York Times. The rate of return on The Social Security Trust Fund is highly correlated to the 10 Year Treasury bond. The rate of return on the 10 Year Treasury bond is highly correlated to how willing institutions are to finance USG deficit spending. The S&P Index gets used as a flash indicator for how well the overall economy is doing. Retirement Funds don’t want to issue negative annual reports for a variety of obvious reasons. Just assume Gauge Invariance, and you can make it look like we live in the best of all possible worlds.

Now we get to where people in finance and economics will eventually feel like cancelling Albert Einstein. To get a legitimate measure of something, you need an honest and fair gauge. The return on an investment is nominally whatever its time series of prices says that it is. But investments don’t really pay off in nominal returns. You live in reality. Whether you eat Milkbones or Filet Mignon in your golden years depends upon real rate of return.

Now, like evil, old Einstein, you are comparing things. Real rates of return are inflation adjusted. Or as Dr. Einstein would have put it they are relative to inflation as all physical rates of change in the universe are somehow relative to c, the speed of light in a vacuum. Thus, we can take our CPI-U as a gauge and see what Sam’s Government claims we are really getting in return for investing in things.

The chart above is considered by a variety of people to be government happy talk. They tend to take CPI-U with a grain of salt. And then perhaps a slice of lime, a dose of tonic, and a shot of Victory Gin. Homebrew Inflation Indexes are then designed based upon what the average mass of people tend to buy over a given period of time.

The Freebuck Index does just such an experiment. As does the more famous Shadowstats CPI-U. The econ student in me goes with Freebuck over Shadowstats for the reason that it makes a less radical claim. It runs 3-3.5% percent “hot” compared to Shadowstats which seems to run about 7%. It’s a lot easier to get away with stealing fewer pennies on the dollar via currency debasement. Using the Freebuck Index as a gauge, we get a look at why otherwise rational people would take more interest in economic radicalism. As you can see below, the weather could be getting pretty nasty out there.

The first striking conclusion is that T-Bills get ruined if the Freebuck Index is an accurate gauge. This is bad for retirees on Social Security. It is awesome for the USG if it can continue selling T-Bills. The ability of the USG to sell T-Bills is at least partially correlated with ROI. This could explain why the official CPI-U runs way cooler that every Homebrew Index I’ve seen. Low official inflation makes Social Security look secure and it makes financing the debt look like a viable, low-loss hedge against market risk.

The second conclusion is that the S&P 500 doesn’t keep up. This may or may not be a result of the one year that the S&P lost 37% because of the mortgage crisis. The chart suggests that this isn’t the case. That would imply the risk inherent in equities markets doesn’t justify the returns they provide.

Finally, a well-managed pension fund (the TSP Index) only barely keeps you ahead. It looks like people would like to think they get from a savings account. Some wicked money management skills and timing can keep you slightly ahead of the Freebuck Index. This seems like a reasonable explanation for why so many people are not getting ahead. Getting ahead is a whole lot harder than the CPI-U makes it out to be.

Einstein would tell us that this is because the laws of physics are equally valid on all equally accelerated entities anywhere in the universe. He would then conclude by telling us that when those laws catch up to your wallet the consequences can end up being a relative b!tch. Perhaps the entire purpose of the CPI-U is to forestall the day when those very same laws catch up to the US Treasury.

Tags: fiat currency, interest, relativity

![]()

- Popular

- Crowdism

- Ethnomasochism

- The Increasing Mediocrity Of Everything

- The Alt Right Is Tired Of Living In Mordor

- Nihilism Is The Basis Of Conservatism

- The Nationalism FAQ

- Beyond the Absolute

- Conservationism Versus Environmentalism

- The Self-Inventing Totalitarian State

- The Biological Basis Of Race

- Whites Going Their Own Way

- How Individualism Defeats Conservatism