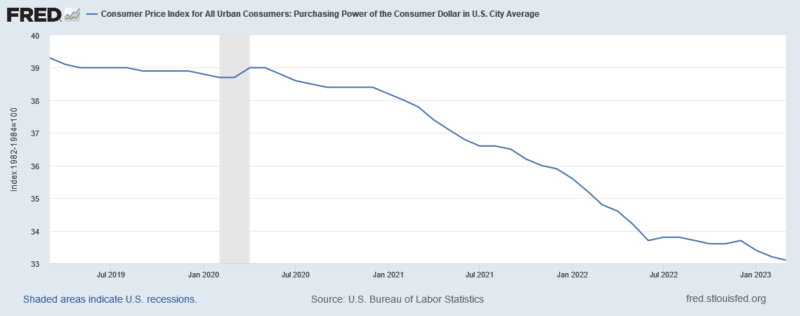

Diversity Impoverished the American People

(October 23rd, 2023) by Brett Stevens | Comments.

Running a Two-Speed World

(June 7th, 2023) by Johann Theron | Comments.

Biden Uses ESG to Devastate the American Economy

(April 23rd, 2023) by Brett Stevens | Comments.

One Way for Conservatives to Seize Power: Crash the Economy

(April 21st, 2023) by Brett Stevens | Comments.

What’s A Petrodollar And Where Did It Come From?

(April 18th, 2023) by Jonathan Peter Wilkinson | Comments.

As Dot-Com Bust 3.0 Arrives, It Comes With a Twist

(August 20th, 2022) by Brett Stevens | Comments.

Remote or Resign

(September 17th, 2021) by Jonathan Peter Wilkinson | Comments.

Dot-Com 3.0 Collapse Back in the News

(July 21st, 2021) by Brett Stevens | Comments.

The Four Horsemen: Part III – The Hedonic Treadmill

(December 10th, 2019) by Jonathan Peter Wilkinson | Comments.

How Trump Has Improved The Condition Of Normal Americans

(October 10th, 2019) by Brett Stevens | Comments.